MagnifyMoney

While a penny saved may be a penny earned, where you keep that penny can determine its purchasing power in the future. In fact, stashing your cash in the right spot is key to maximizing your money — otherwise, you run the risk of your money losing its value over time due to inflation.

However, a new MagnifyMoney survey of over 1,000 respondents reveals a disheartening reality: Nearly 1 in 4 consumers have “no idea” where to put their money. This is especially true for Gen Xers and high-income households. Additionally, we found that the majority of consumers are simply keeping their cash in checking accounts, which are notorious for doling out dismal interest rates.

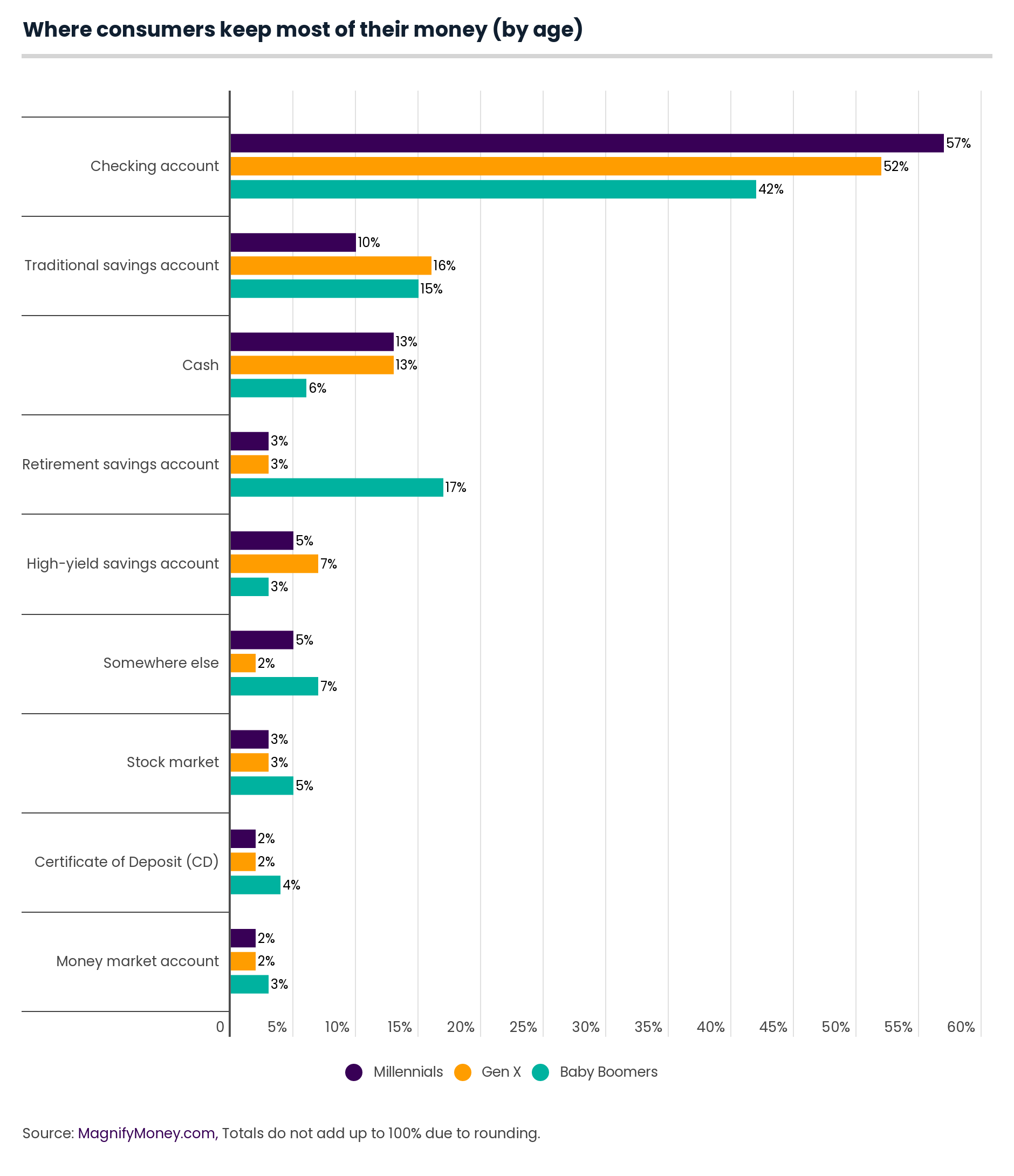

When it comes to maximizing your money, standard checking accounts are not the best spot to stash your cash, as they are currently doling out an average APY of just 0.121%. Still, our survey found that checking accounts are by far the most popular place for consumers to keep their money, with a staggering 50% of respondents saying they keep the majority of their money in checking. Overall, millennials and women were more likely than other demographic groups to stash their cash in checking.

While checking accounts certainly offer benefits like flexibility and convenience — often by allowing unlimited withdrawals and transfers — they pale in comparison to other accounts in terms of interest or returns earned. Not surprisingly, our survey found that the most common reason that people keep their money in a checking account is convenience.

The second most common place for people to keep their money is in a traditional savings account (14%), with men more likely than women to keep their money in traditional savings, and Gen Xers more likely than millennials and baby boomers. Understandably, as savings accounts are more liquid than other types of accounts like brokerage accounts or even CDs, the most cited reason for keeping the majority of their money in a traditional savings account was “to ensure I can access it in the case of an emergency.”

Interestingly, while high-yield savings accounts offer many of the same benefits as traditional savings accounts, such as liquidity and convenience, survey respondents were far more likely overall to say they keep most of their money in traditional savings accounts (14%) as opposed to high-yield savings accounts (5%).

Meanwhile, we found that the third most common place for consumers to keep their money was simply in cash (10%). Men, millennials and Gen X were the most likely to keep their money in cash. This is especially concerning, as over time, cash can erode in value due to inflation, while other savings vehicles — think brokerage accounts and retirement savings accounts — are not only known to keep pace with inflation, but to outearn it through compounding returns.

While our survey found that most consumers are already keeping their funds in checking accounts, traditional savings accounts and as cash, we also discovered that even if people were to receive a windfall, many would not change their savings habits — despite potentially receiving much higher returns elsewhere.

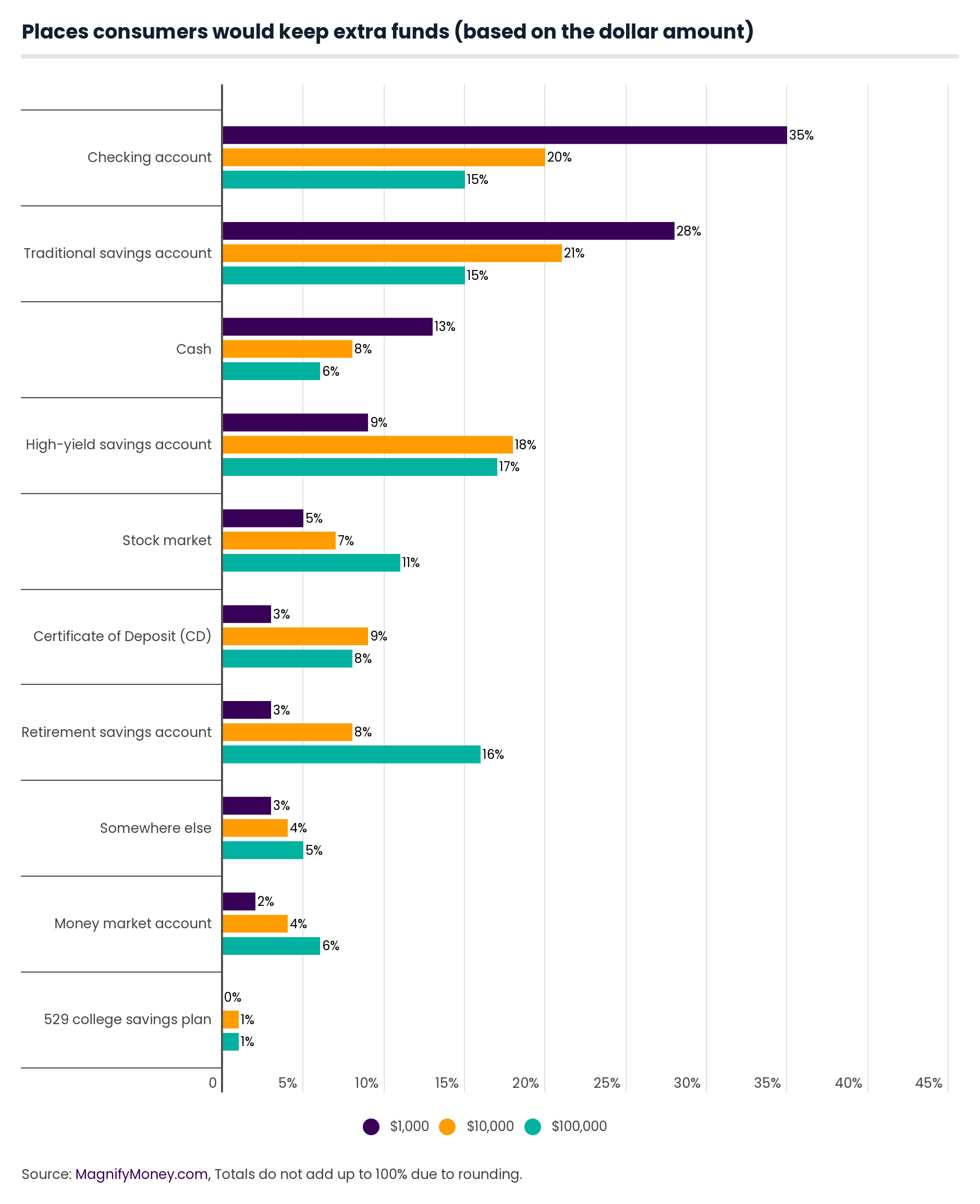

We found that if people were to receive an extra $1,000, they are most likely to put it in their checking account (35%), followed by a traditional savings account (28%) and as cash (13%). That trend continues for even larger dollar amounts, with the top place for putting an extra $10,000 being traditional savings accounts (21%) followed by checking accounts (20%). That tune starts to change with windfalls of $100,000 — in that case, the top spot is a high-yield savings account (17%) followed by retirement savings accounts (16%).

Still, our findings underscore a concerning pattern: Older consumers are far more likely to keep their funds in savings vehicles that need more time to generate lucrative returns. For example, we found that baby boomers were far more likely (23%) than Gen Xers (14%) and millennials (15%) to put an extra $100,000 in their retirement savings fund despite being decades closer to their retirement years and having less time for their returns to compound.

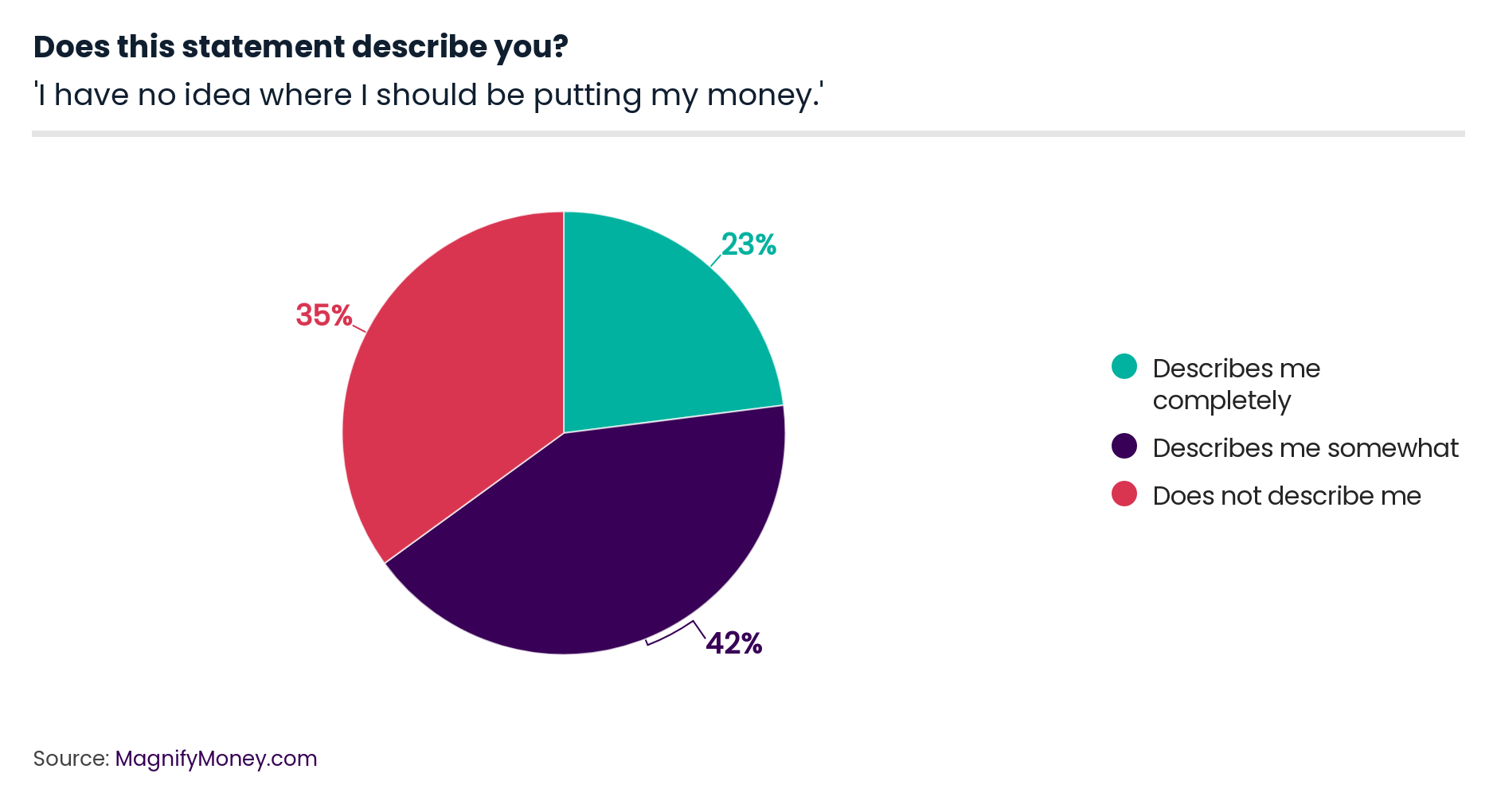

Our survey’s findings suggest that one potential reason that so many consumers store their money in low-yielding accounts could be a lack of knowledge. According to our survey, 23% of consumers feel like they have no idea where they should be putting their money, and a marked 42% of consumers said that they “somewhat” feel that way, too.

We found that men were much more likely (33%) than women (14%) to say that they have no idea where to put their money, as were Gen Xers (43%) when compared to baby boomers (11%) and millennials (22%). Additionally, we found that households making at least $100,000 were more likely than households with lower annual incomes to be uncertain about where to stash their cash.

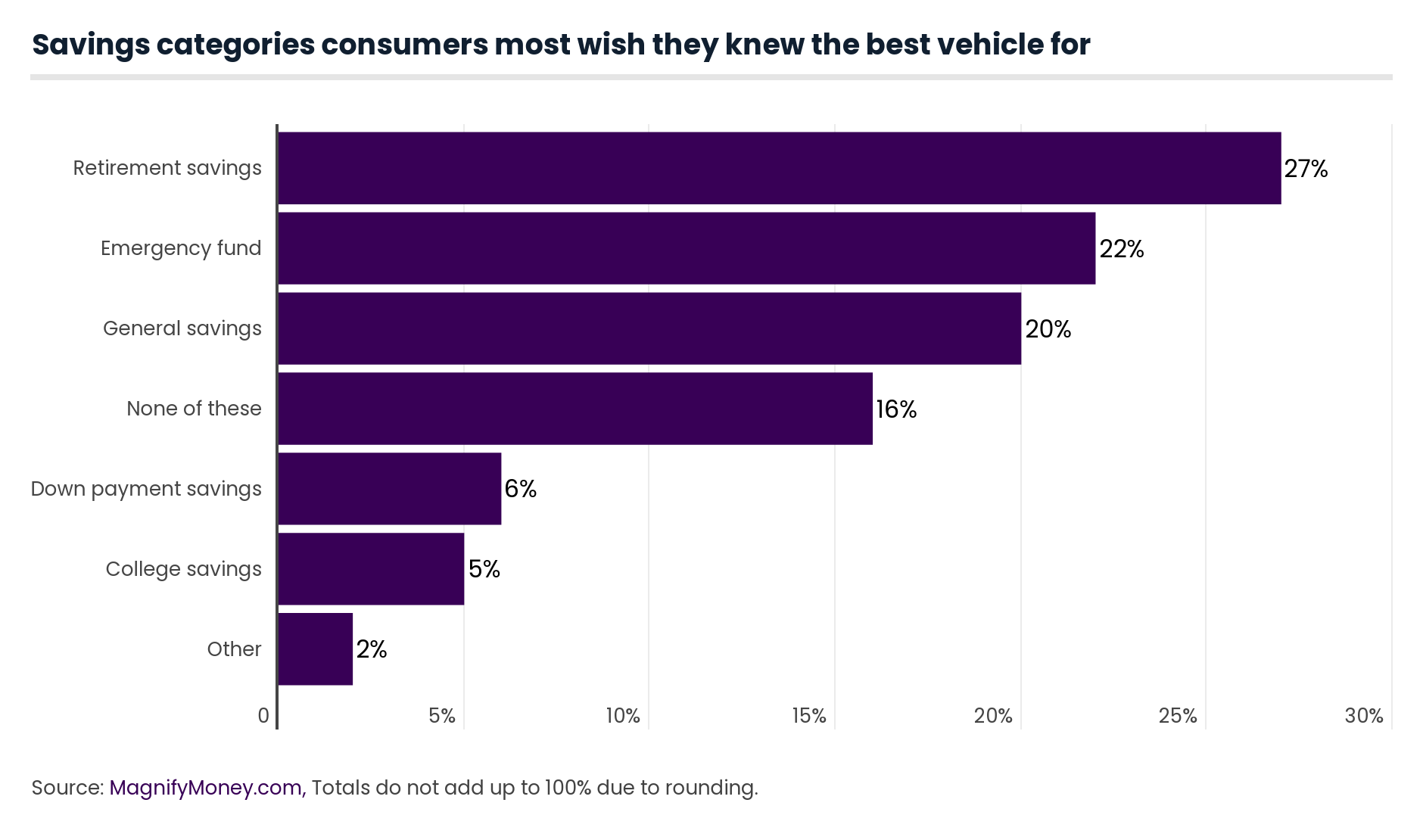

Overall, we found that retirement savings, emergency funds and general savings are the three savings categories that people wish they knew more about how best to save for in terms of the most appropriate savings vehicle.

Many experts agree that retirement savings should be socked away in retirement-specific savings vehicles, such as 401(k) plans or Roth plans, but determining where to put other savings can be difficult, especially in a low-rate environment. However, DepositsAccounts founder Ken Tumin says that even the small rate difference between traditional savings accounts and high-yield online savings accounts makes a difference.

“The current low-rate environment has made online savings accounts less attractive,” Tumin admits. “The rate advantage over standard checking accounts and savings accounts has diminished. Nevertheless, there is still a rate advantage, and that rate advantage will once again grow in the future when rates eventually rise. It still makes sense to keep money that’s intended to be used for short-term goals or an emergency fund in an online savings account.”

MagnifyMoney commissioned Qualtrics to conduct an online survey of 1,029 Americans, with the sample base proportioned to represent the overall population. The survey was fielded on August 25, 2020.

For the purposes of our survey, generations are defined as the following ages in 2020:

Note that while survey responses from Gen Z (age 18-23) and the silent generation (age 75 and older) were factored into the overall percentage totals among all respondents, they were omitted from generational comparisons due to the low sample size among both groups.

Sarah Berger

Sarah BergerSarah Berger is a former writer at LendingTree, where she covered personal finance, specifically focusing on challenges and opportunities facing millennials. Before joining LendingTree, she was a writer for CNBC and Bankrate.

Read More