MagnifyMoney

Earning your college degree can open the door to more career opportunities and a higher income. But, as a recent MagnifyMoney study points out, college degrees are more valuable in some metropolitan areas than in others.

Where you live has a major impact on your income, both during your working years and after you retire. Correspondingly, college degree holders in some cities are more likely to find employment, become homeowners or secure health insurance coverage than their peers elsewhere.

We examined income, employment and related data for degree and non-degree holders across the 50 largest metropolitan areas in the U.S. and ranked each area from 0 to 100. This “final score” represents the overall value of a bachelor’s degree in each area.

Here’s what we discovered about where a college degree matters most.

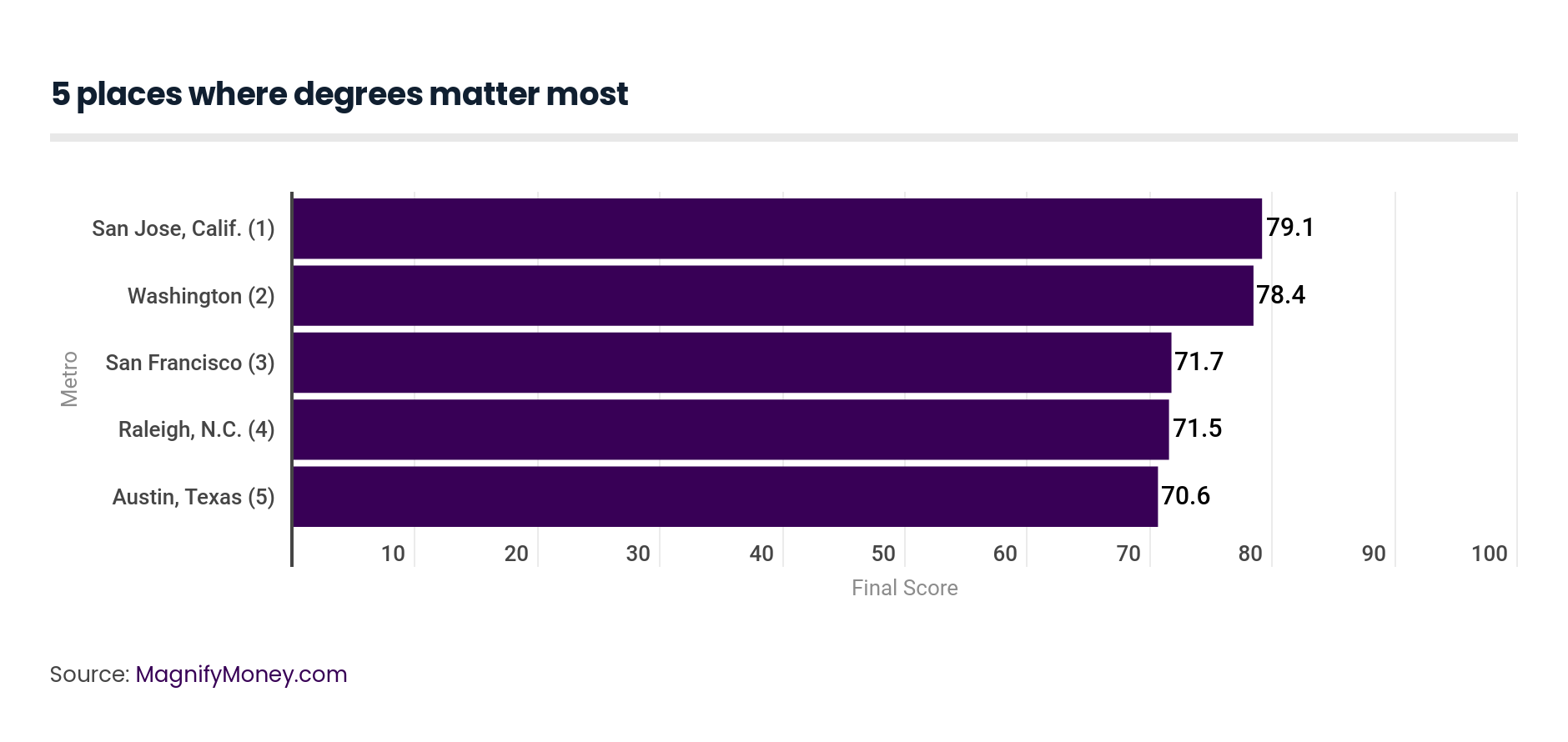

Based on the study, the earnings-and-opportunities premium for those with college degrees seem most pronounced in wealthy and highly educated cities. The five places where degree-holders’ incomes outperformed were:

A college degree remains a valuable asset for professionals, even when considering the student debt that often goes with it. On average, people with a bachelor’s degree make $22,422 more than those with only a high school diploma, as well as $16,682 more than those who attended some college or even received an associate’s degree.

But the difference is most pronounced in certain areas, such as San Jose, Washington, D.C., and San Francisco. As noted above, San Jose tops the list for places where college degrees are the most valuable. In this Californian city where nearly half the population has a bachelor’s degree or higher, the median income for degree holders is 83.6% above that for non-degree holders.

San Jose residents with college degrees also don’t seem to have a ton of student debt dragging down their finances. The ratio of median student loan balance to median degree-holder income was just 18.6%, the lowest of any metro area included in this study.

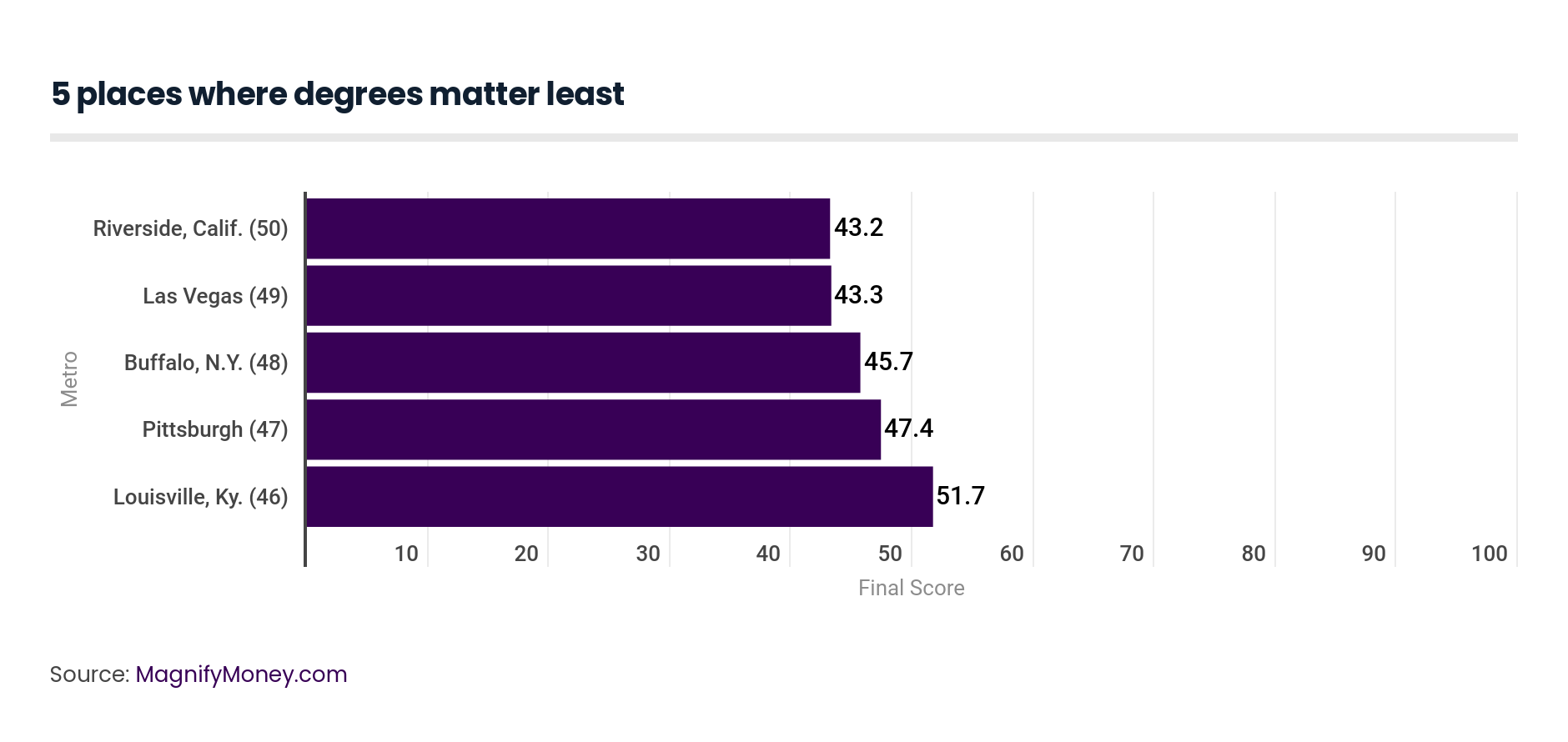

On the flip side, a college degree doesn’t correlate with a major boost in income in all areas. In Las Vegas, where 22.8% of the residents have a bachelor’s or higher, a degree only increases median income by 16.9%. In Riverside, California, the increase is just 20.4%.

Both these figures are well below the overall average of 53.9%. Plus, the ratio of median student loan balance to median income was 52.5% in Las Vegas and 58.2% in Riverside. So not only do residents see a lower return on investment from their degrees, but they also end up with burdensome student loan debt that’s difficult to pay off.

A relatively smaller salary and larger debt creates other problems, too. For example, if you’re hoping to use student loan refinancing to lower your interest rate or reduce your monthly payments, you’ll have more trouble qualifying for refinance with less pay and a heavier debt load.

It appears that differences in cost of living or earning opportunities can impact the value of a college degree to a major extent. Although a college degree increases earning potential anywhere, its effects are much stronger in some areas than in others.

Although a four-year degree’s effect on income varies by location, its impact on funds for retirement appears to be more steady. Overall, college degree holders have an average of 42.2% more in retirement income than those without a degree. This figure only changes by about 10 percentage points or less when factoring in location.

Retirement income refers to the money you have coming in after you retire. This could come from retirement savings, but it might also come from other assets, insurance, inheritances, stocks, pensions or Social Security allowances.

Surprisingly, having a degree only meant a 34.4% boost in retirement income in San Jose, the city where degree holders chalked up the biggest jump in income. The only city where a degree was even less valuable in terms of retirement income was Cleveland, where degree holders received an average of 32.2% more in median retirement income.

So why are people with degrees in areas like Cleveland only making 32.2% more than those without degrees, while those in other cities, such as Austin, get an average of 52.9% more? One key difference might be the availability of blue collar and government jobs with pensions.

Certain areas might provide more public sector jobs and other employment opportunities that come with pensions but don’t require college degrees. In those cities, non-degree holders might be better financially protected, even if they don’t have as high an earning potential as those with degrees.

Unfortunately, pensions in the private sector have become less and less common, and there’s no guarantee that even public sector pensions will continue to be available in the future. For now, though, they seem to be helping retired degree and non-degree holders alike, albeit in certain cities more than others.

Earning your bachelor’s doesn’t just open the door to higher-paying jobs; it also increases your chances of gaining employment at all. According to our study, degree holders are 52.7% more likely to be employed than non-degree holders.

Holding a college degree was most useful in Birmingham, Baltimore and Milwaukee, where degree holders were 63.7%, 63.7%, and 62.9% more likely to be employed, respectively.

On the other side of the spectrum, it had the lowest effect in Austin (35.4%), Los Angeles (39%), and Denver (40.5%).

According to the Bureau of Labor Statistics, a higher level of education corresponds with lower unemployment across the U.S. Bachelor’s degree holders had the lowest unemployment rate of 2.1% in April 2018. The data showed jobless rates rising for workers at lower education levels: 3.5% for people with some college education, 4.3% for high school graduates, and 5.9% for those without a high school diploma.

That said, employment opportunities vary by location, and some cities host industries that have little presence elsewhere. So while your education level impacts your chances of employment, so too does the metropolitan area in which you live.

Since higher education can lead to a higher income, it should come as no surprise that degree holders are also more likely to own homes. Overall, college graduates are 21.8% more likely to be homeowners than non-college graduates.

In San Antonio, bachelor’s degree holders are 40% more likely to be homeowners. In Las Vegas, having a degree correlates with a 33.7% greater chance of owning a home, and in L.A. it comes with a 31.4% greater chance.

That said, having your degree doesn’t necessarily mean you’re more likely to own a house. In Pittsburgh, degree holders are only 0.7% more likely to be homeowners. And in Buffalo, that likelihood is only 11.3% higher.

Lots of factors play into homeownership, including the average age of the local population, how much student debt residents have and of course, the cost of real estate itself. In some areas, low prices might make it easier for all residents to buy homes, regardless of whether they hold a college degree and receive the higher income that often goes with it.

On the flip side, high costs of living could make homeownership cost-prohibitive for everyone, especially if degree holders are paying off large amounts of student debt. With high student loan payments, graduates might be wary of taking on a mortgage — or might not have the financial credentials to qualify in the first place.

The U.S. has an employer-based health insurance system, meaning many of us rely on our employers to provide coverage. Since employers tend to subsidize health care costs, employer-sponsored plans are typically the most affordable.

Since we saw that college degree holders tend to have higher rates of employment, as well as bigger salaries, it follows that they’re also more likely to have health insurance. The difference is not particularly dramatic, though: Overall, those with degrees are just 11.5% more likely to have health insurance.

The gap is most evident in Houston, Dallas and Miami, where college graduates are 20.1%, 18.2%, and 18.1% more likely than non-college graduates to have coverage, respectively. But in Buffalo, Boston and Providence, the difference is minimal, with the relative likelihood at just 4.4%, 4.5%, and 5.9%, respectively.

One variable to consider is the availability of state-sponsored health insurance. For instance, Massachusetts has MassHealth, a state-run program that provides affordable health insurance to low-income residents. If your state has a similar program, you might not need employer-sponsored health insurance if you meet eligibility criteria. But if not, you could be facing high premiums without the help of an employer.

With the high rates of student debt in the U.S. — $1.48 trillion at the latest count — it’s natural to feel skeptical about the value of a college degree. But even with the student loans that often accompany higher education, a college degree remains valuable across the country.

Not only does it correlate with higher income, but it also boosts your chances of employment. Plus, having your degree could lead to higher retirement income, an increased chance of homeownership and a greater likelihood of health insurance coverage.

That said, the value of a degree isn’t the same everywhere. Some cities might be home to industries that look for college degree holders, while others might not have as many employment opportunities or high-income careers.

If you’re looking for the greatest return on investment for your degree, consider moving to an area with job opportunities in your current field. Cost of living might be another important factor when choosing where to live, as it could have a big impact on your chances of becoming a homeowner.

By being selective about where you reside, you can leverage your college degree into a high-paying career, as well as a higher income after you retire. Not only will earning your college degree likely lead to greater financial stability but optimizing where you live can also help put your degree to work for you.

This study was conducted by Prabhat Kumar and Aditya Patil. It was limited to the 50 largest statistical metropolitan areas by population, and measured differences between people ages 25 and older with and without four-year degree educations or higher. Six metrics were scored from 0 to 100: ratio of median loan balance to median income for degree holders; difference in median incomes between degree holders and non-degree holders; difference in median retirement incomes; difference in unemployment rates; difference in homeownership rates; and the difference in health insurance coverage. These were assigned weights and then combined into one score. Income and rent values were normalized using the Regional Price Parity from the Bureau of Economic Analysis to account for variability in buying power across the MSAs. Data was sourced from 2016 American Community Survey data from the U.S. Census hosted on IPUMS and American FactFinder and from a student loan balance study published in May by LendingTree (our parent company).

Rebecca Safier

Rebecca SafierRebecca Safier is a former student loan reporter for LendingTree.com-owned websites Student Loan Hero and MagnifyMoney.

Read More