MagnifyMoney

Life changes, and often that means finances change, too. A financial advisor can be a valuable guide during these times, clarifying the financial aspects of buying a house, retiring and more. But 42% of Americans think financial advisors are only for the wealthy, even as 95% of those with one say they’re worth the money.

We surveyed more than 1,500 Americans on everything from why they have (or don’t have) a financial advisor to whether they’d consider getting a financial advisor in the future, to whether people think they could get the same information on Google. Here’s what they said.

A paid financial advisor isn’t something the average person has in their corner, with just 30% of respondents saying they have one.

When you look at the demographics:

Once we looked into the who, we asked about the why. For those who have a financial advisor, the most common reason cited was investment management (60%).

Other common reasons included:

Millennials, Gen Xers and baby boomers cited investment management as the main reason why, while Gen Zers cited tax planning. In fact, 46% of Gen Zers with a financial advisor get help with tax planning, versus:

For the most part, those with a financial advisor said they hired one after a specific life event (60%). Getting married or divorced (14%) or receiving an inheritance or other large sum of money (11%) were among the most common responses. Another 12% cited reaching retirement age, but that can be a costly wait in the long run.

“Consulting an advisor earlier in life, when your money has lots of time to compound and grow, could reap you huge gains,” said Ismat Mangla, MagnifyMoney’s content director.

Smart times to seek professional financial advice, she said, include when you’re approaching a decision like buying a house or a major life event like getting married.

“Such events can trigger complex financial issues, and it can be beneficial to have a pro help you navigate them,” she added.

Some interesting trends emerged around this, including:

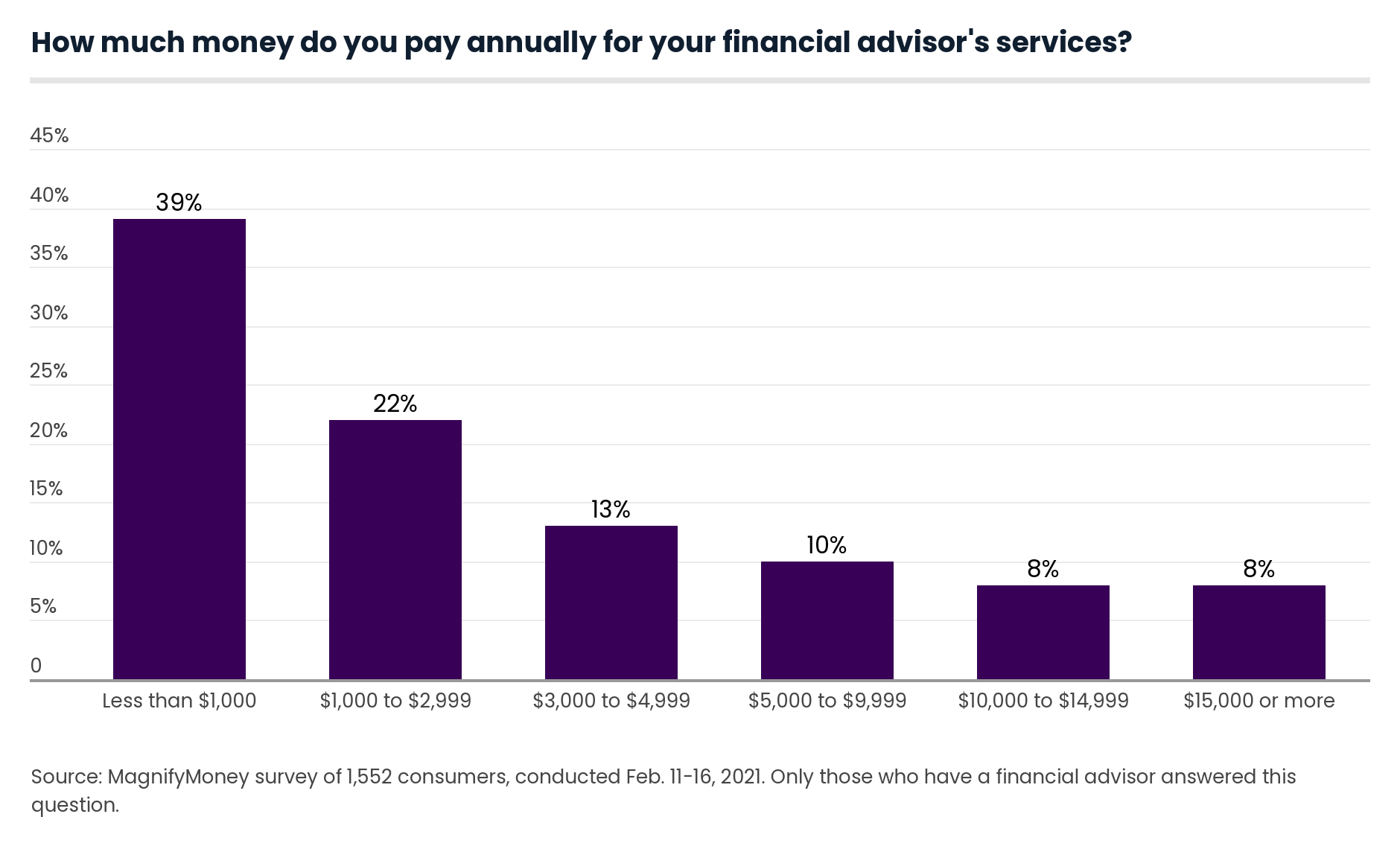

Again, delaying getting a financial advisor can be a bad move in the long term, especially for those who wait until retirement to start thinking about it. But for those who are interested in getting started, it’s important to know that it may be less expensive than many assume. Of those with a financial advisor, more than 6 in 10 pay less than $3,000 annually for those services.

On a positive note, 95% of those with a financial advisor think it’s worth the money. So for those who can afford one — and are nearing an important financial decision — it’s a smart financial move.

To get a more complete picture of public perceptions around financial advisors, we also looked at those who didn’t have one.

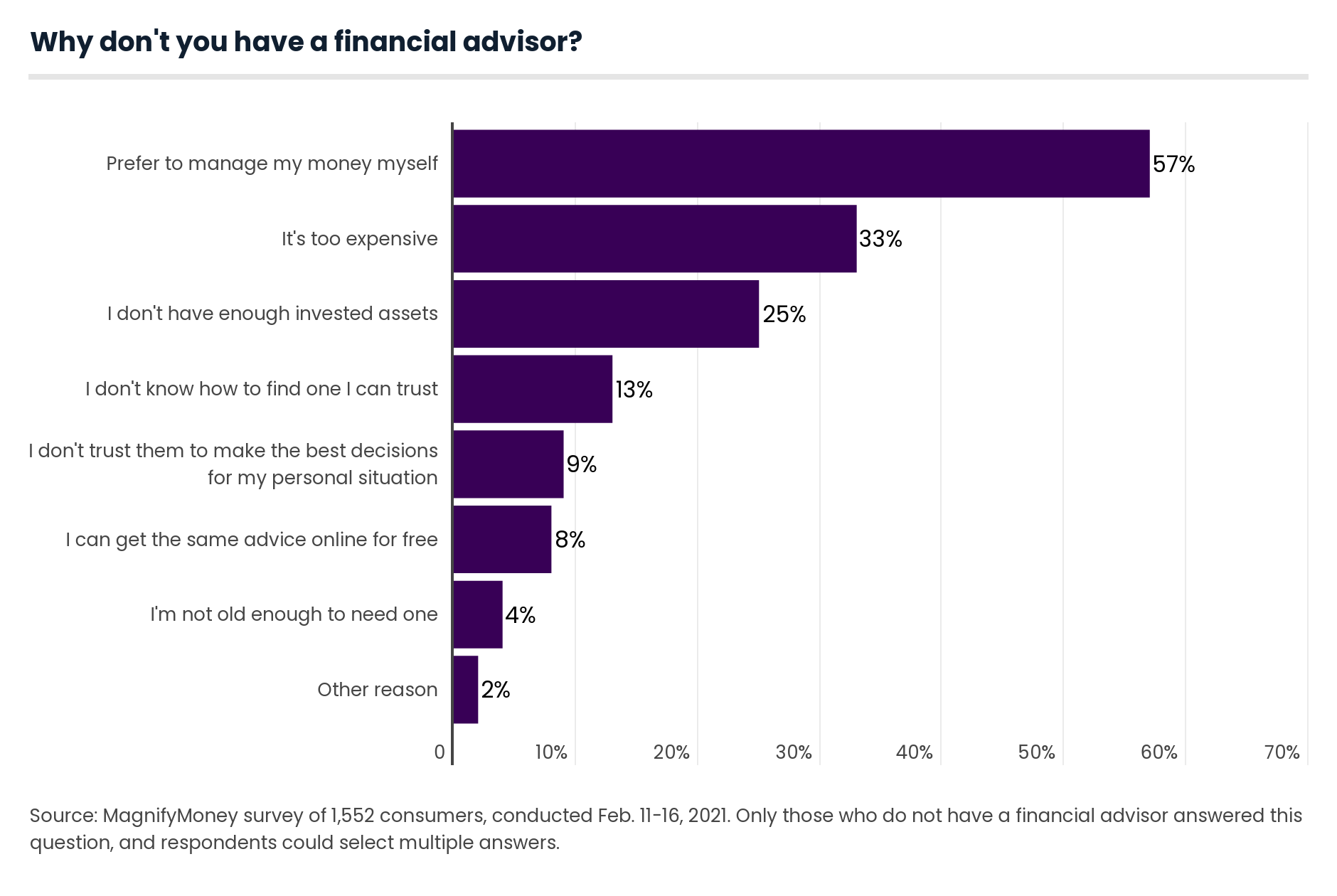

Of this group, 57% said they prefer to manage their money themselves, while 33% believe it’s too expensive and 25% don’t think they have enough invested assets.

We also asked what factors might be important should those in this group opt to get a financial advisor. Unsurprisingly, a lot of it came down to money. In fact, 58% said fair fees would be the most important quality they would look for were they to hire a professional, followed by being local to their area and showing a history of proven returns.

Of note, 12% of millennials and 11% of Gen Zers cited that diversity was important to them, versus 6% of Gen Xers and 4% of baby boomers.

All in all, most of those who didn’t have a financial advisor weren’t opposed to it. In fact, 78% of those without one would consider hiring one at some point. But earnings and assets played a large role in this hypothetical situation. Namely, 28% said they’d hire a financial advisor if they start earning more than $100,000, compared with 24% if they receive a large inheritance and 23% if they have more than $500,000 in investable assets.

Most Americans don’t have a paid financial advisor, and it appears that could have led to misconceptions around the services a financial advisor could provide and when it’s a good idea to get one.

For example, 42% of those surveyed think financial advisors are only for wealthy people. This was more prevalent among women (48%) than men (35%).

Another interesting aspect was timing, as 25% of respondents said they think you don’t need a financial advisor until you’re middle-aged. Unsurprisingly, this was more common with younger generations. In fact, 44% of Gen Zers thought this, compared with:

In the same vein, the cost of financial advisors was another point of misunderstanding. In fact, 45% of those who don’t have a paid financial advisor — and 50% of consumers in general — think they typically cost much more than they do. For context, fee-only advisors typically charge between 0.5% and 1.25% of the assets they manage.

This overestimation of cost is likely a major factor as to why so many forgo getting a financial advisor in the first place. But consumers should be aware, Mangla said, that a fee-for-assets model isn’t the only option. You could seek out an hourly or per-project fee structure as well.

Ultimately, it seems that most people (whether they have a financial advisor or not) place value on the ability to have a real person managing their finances.

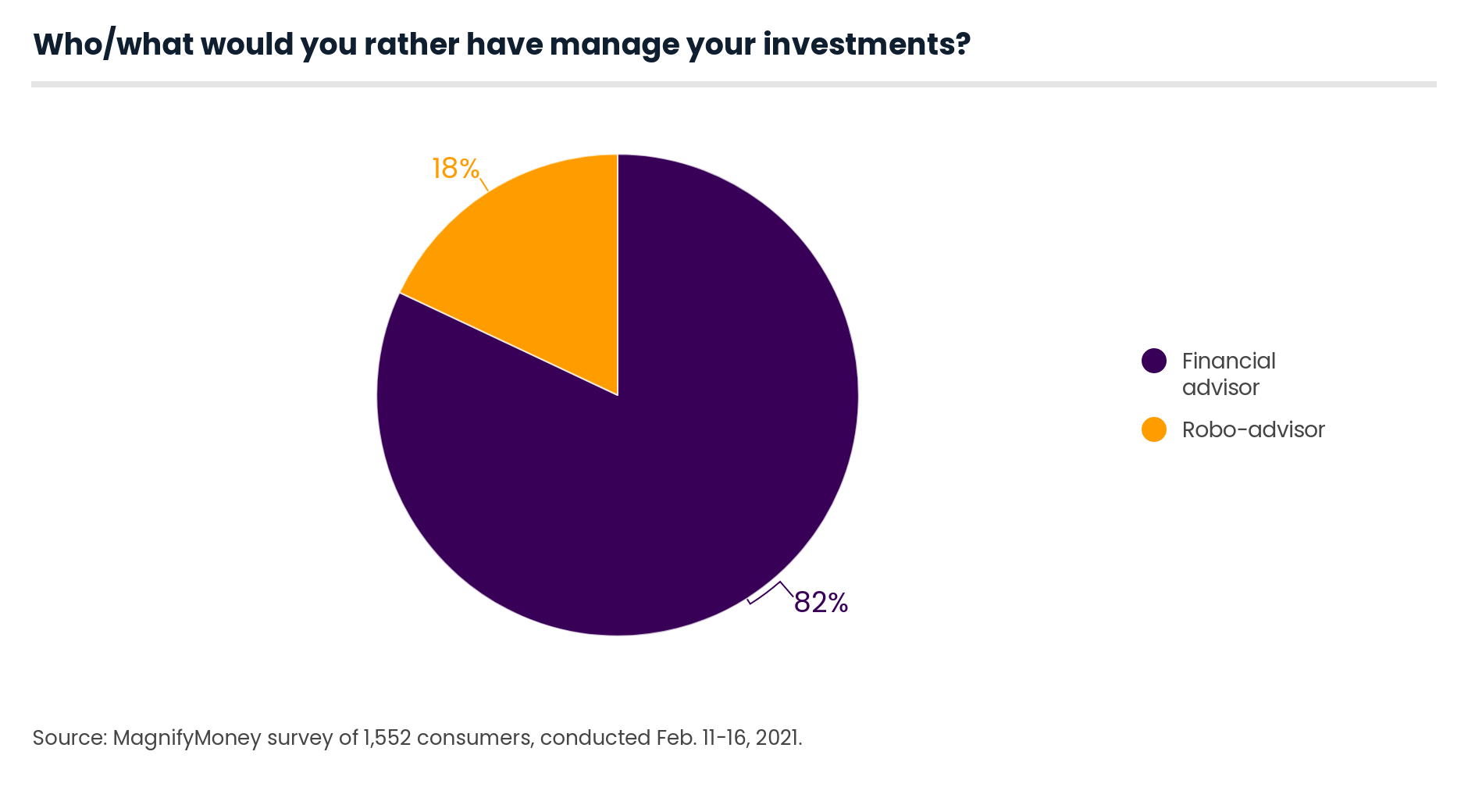

Our survey found that 82% of respondents would rather have a financial advisor manage their investments than a robo-advisor.

The main differences came from Gen Z (29% said they’d prefer a robo-advisor, more than any other generation) and those making less than $35,000 (a higher proportion said they preferred a robo-advisor compared with higher earning brackets).

Lastly, while most people think that Google isn’t a sufficient replacement for information a financial advisor could provide, a significant 38% did agree with that statement. This idea is also more prevalent in younger demographics: Nearly 50% of those 40 and younger believe this.

However, it’s important to note that a financial advisor’s role isn’t always as simple as some would believe, and depending on the complexity of your finances, having an expert in your corner can be valuable.

“Before you start shopping around for an advisor, make a clear list of the problems you want to solve or the goals you want to achieve,” Mangla said. “That can help you find the right financial help.”

MagnifyMoney commissioned Qualtrics to field an online survey of 1,552 Americans, conducted Feb. 11-16, 2021. The survey was administered using a non-probability-based sample, and quotas were used to ensure the sample base represented the overall population. All responses were reviewed by researchers for quality control.

We defined generations as the following ages in 2021:

While the survey also included consumers from the silent generation (defined as those 76 and older), the sample size was too small to include findings related to that group in the generational breakdowns.

Devon Delfino

Devon DelfinoDevon Delfino is an independent journalist with work featured in the Los Angeles Times, U.S. News & World Report, Teen Vogue, Forbes, MarketWatch, CNBC and USA Today, among others.

Read More