MagnifyMoney

The holiday season is a time for celebrating and exchanging gifts with loved ones — which can often mean swiping credit cards or taking on loans in the process. About a third (31%) of all consumers took on debt to pay for holiday expenses this year, according to a December 2020 MagnifyMoney survey of 1,171 Americans. Holiday debt was defined as spending related to gifts, travel and entertainment.

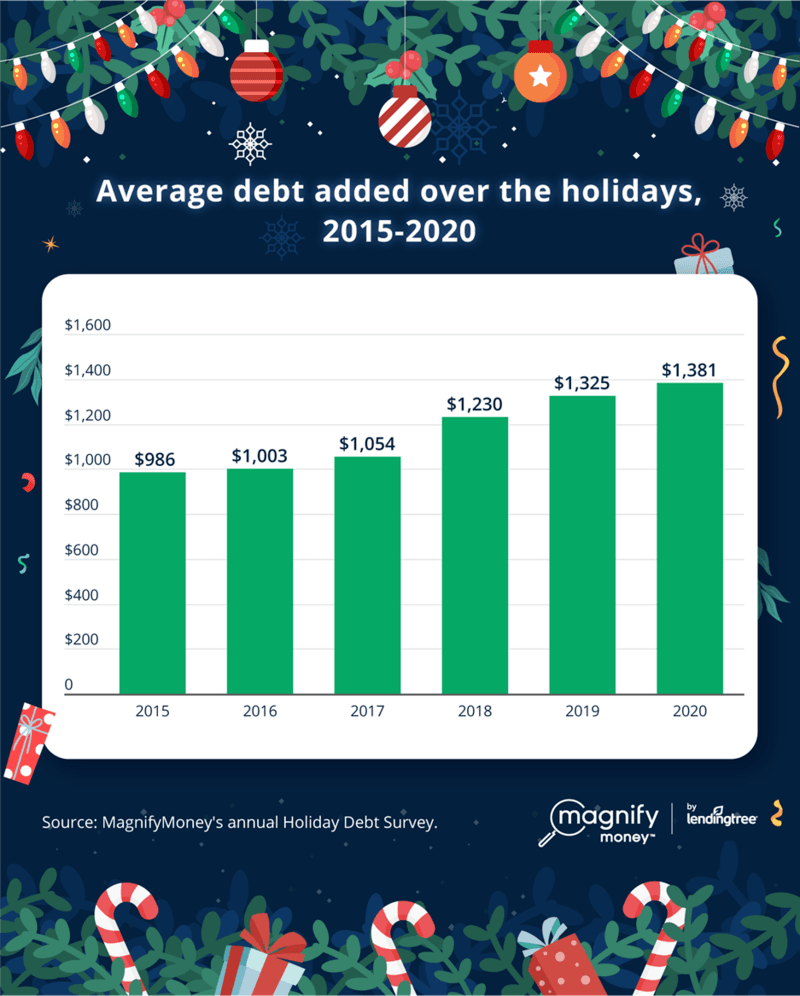

Those who incurred holiday debt this year borrowed $1,381 on average. That’s up from $986 in 2015, an increase of nearly $400, or 40%, since we first started conducting this survey five years ago.

As the coronavirus pandemic continues to shape how we earn and spend money, fewer Americans racked up holiday debt than last year, but the ones who did — often millennials and parents of young children — borrowed more money than ever before.

See what else we uncovered in the report below.

Fewer Americans took on holiday debt to pay for gifts, travel and entertainment in 2020 than they did in 2019, at 31% versus 44%. However, those who did incur debt over the holidays borrowed more money on average. See how holiday debt has steadily increased since we began this survey in 2015:

“The pandemic has wrecked so many things for so many people, canceling birthday parties, vacations, family get-togethers and more,” said Matt Schulz, chief credit analyst at LendingTree. “Now, many people are likely trying to overdo it a bit for Christmas to make up for a crummy year. It’s easy to understand, but that spending can really clobber your budget.”

Borrowing money is an added cause of anxiety during the holiday season. Most (66%) consumers who borrowed money for the holidays are stressed about their debt. Among the most stressed were parents with young children and millennials, at 73% each. Americans in these demographic groups also took out debt at the highest rates.

The indulgent holiday season is commonly followed by resolutions of doing better in the new year. In fact, getting rid of debt is Americans’ most popular financial resolution for 2021, according to a recent MagnifyMoney survey.

Still, most consumers will likely not take advantage of debt payoff strategies like debt consolidation or balance transfers. Less than two in five (38%) consumers with holiday debt will try to consolidate their debt or shop around for a good balance transfer rate. For those who will not, the most common reason was not wanting to deal with another bank (20%).

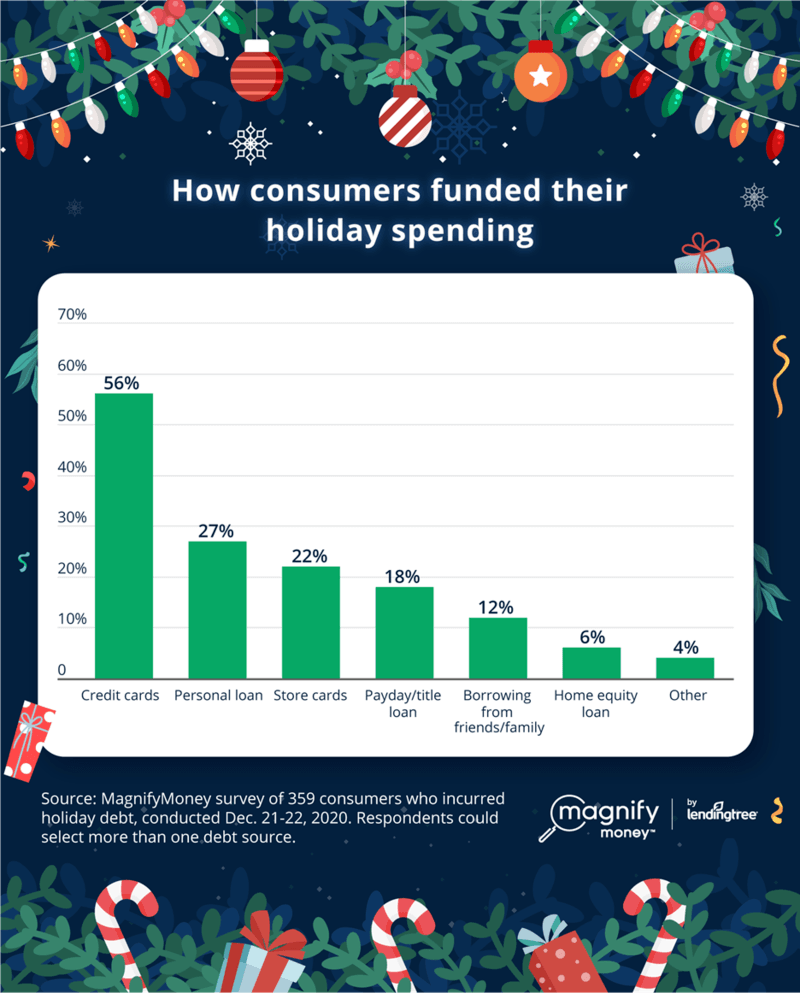

The majority (56%) of those who took on holiday debt used a credit card to finance their purchases. About half as many took out a personal loan for holiday spending.

Some borrowers turned to riskier sources: 18% of those who borrowed money to pay for holiday expenses financed their spending with a payday or title loan, up from 11% in 2019. Payday loans often come with triple-digit APRs and short repayment periods, leaving borrowers trapped in a cycle of debt they can’t repay. Auto title loans use a vehicle as collateral, putting borrowers at a high risk of having their car repossessed.

Plus, more than a fifth (22%) took on debt using a store credit card, which can come with sky-high interest rates.

Of those who borrowed money to pay for holiday purchases, 89% say they won’t be able to pay off that debt in a month. Credit card users in particular are likely to pay interest on their holiday purchases, since they’ll be carrying a balance from month to month.

“That’s an awful lot of people carrying over balances for a while,” Schulz said. “That tells me that these folks aren’t just taking on debt for convenience’s sake or to run up rewards. They’re doing so because they don’t have any choice.”

Additionally, about a fifth (18%) of consumers with holiday debt said they only plan on making minimum payments on that debt.

It would take more than five years to pay off $1,300 making minimum monthly payments of $31 with an interest rate of 14.5%. Plus, you’ll pay more than $600 in interest — almost half the original debt itself — by the time you’re done paying it down, years after the holiday has ended.

It’s worth noting that many consumers could take even longer to pay off their debt and pay more in interest charges, since 23% of consumers who took on holiday debt noted their APR was 20% or more.

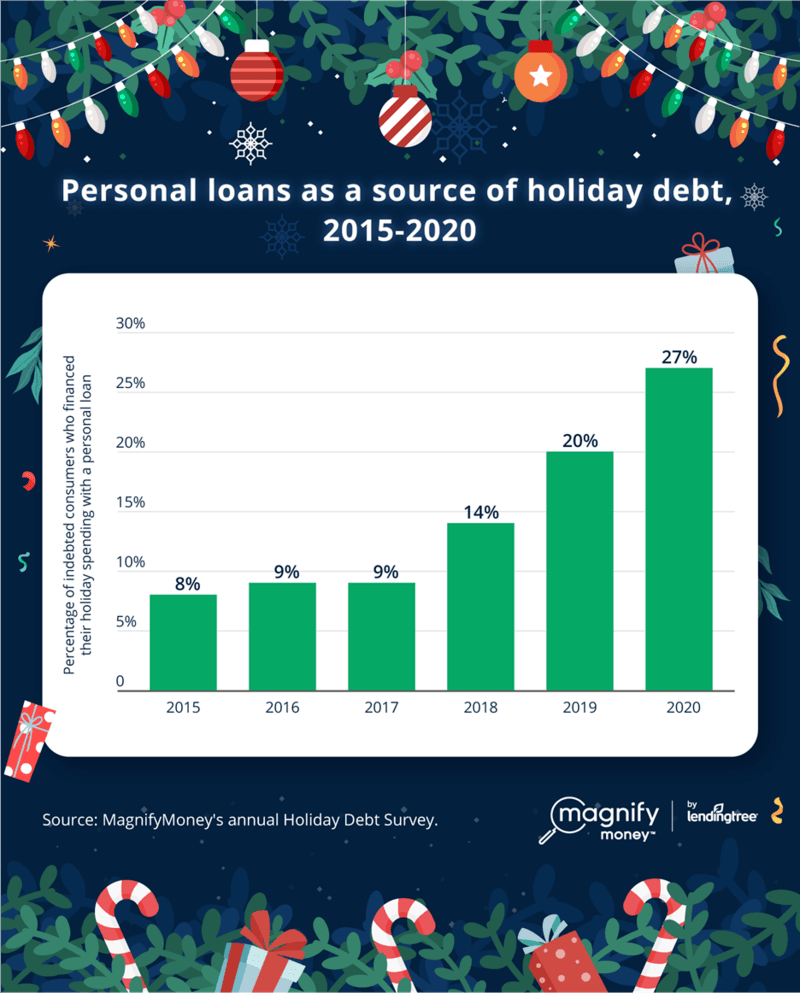

Consumers are increasingly using personal loans to finance their holiday spending. More than one in four (27%) consumers who took on holiday debt this year said that debt came from a personal loan, up from 20% last year. That’s an increase from just 8% in 2015, when MagnifyMoney first conducted this survey.

“Personal loans are booming as an alternative to credit cards,” Schulz said. “They’re a good, simple option for folks who want to finance a purchase but don’t want to mess with a credit card.”

Borrowers with good-to-excellent credit may find personal loans to be a cheaper alternative to credit cards, since they typically qualify for lower APRs than they would with a credit card. Personal loans also have fixed APRs and are repaid in fixed monthly installments, giving borrowers a clear picture of when they’ll pay off their debt.

However, shoppers should be wary of using a personal loan to pay for unnecessary expenses like holiday purchases. While personal loans may sometimes be a better alternative to credit cards, it’s still best to budget your money and save up in advance to avoid paying financing charges like interest and loan fees on nonessential purchases.

Nearly two in five (37%) Americans turned to point-of-sale companies like Affirm and Quadpay to break up their holiday purchases into smaller payments in 2020. About a fifth (21%) of consumers utilized special financing for multiple purchases this holiday season.

Point-of-sale financing, also known as “buy now, pay later,” lets consumers break their purchases into smaller installments upon checkout. These point-of-sale agreements are typically either interest-free installment plans or small unsecured loans, some of which carry APRs as high as 30%.

“Point-of-sale financing hit critical mass in 2020 and is likely here to stay,” Schulz said. “People like it because the payments are typically predictable and easier to understand than credit card payments, and there’s no risk of running up more debt after the loan is paid off.”

Americans under 40 were far more likely to utilize “buy now, pay later” agreements to finance their holiday purchases than their older counterparts, as indicated below:

While some point-of-sale companies let you break your purchase into smaller, more digestible payments without charging interest, that’s not always the case. Some charge interest and late fees, both of which increase the cost of holiday shopping.

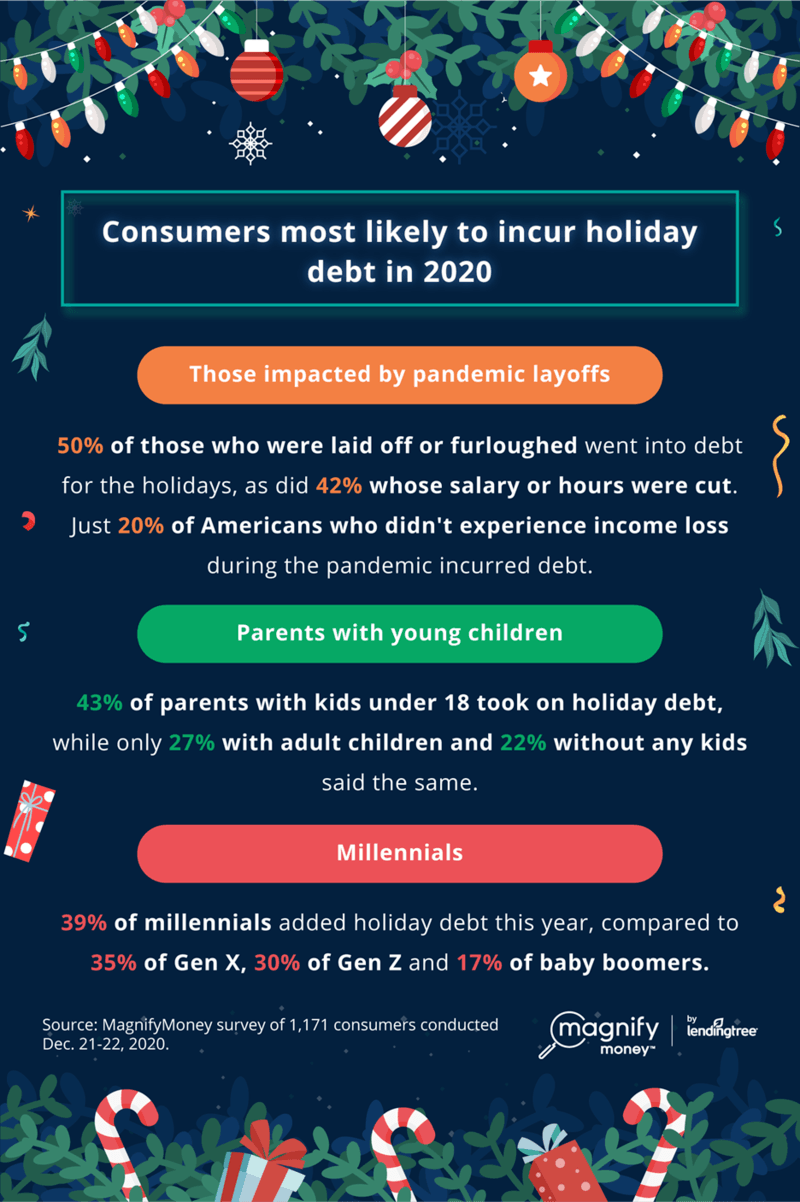

The coronavirus pandemic has been a source of financial stress for many Americans, and there’s no exception when it comes to holiday spending. Half of those who were laid off or furloughed due to the coronavirus pandemic took on holiday debt.

Consumers who lost income due to the coronavirus pandemic were more than twice as likely to take out holiday debt than people whose incomes were not affected by the pandemic.

The holidays are a time of increased spending for many people, but parents with young children are hit particularly hard. Parents with kids under 18 were twice as likely to take on holiday debt than Americans with no children, at 43% and 22%, respectively.

“Parents with young children are always at risk of taking on more debt during the holiday season,” Schulz said. “There’s so much pressure from all sides to get just the perfect gift that often budgets are wrecked in a big hurry.”

Schulz also suggested that parents are overspending to make up for a tough year. 2020 has been particularly hard for young children and their parents alike, who have had to adapt to learning virtually, wearing masks and staying socially distant. While it makes sense that parents want to spend more money this holiday season, they should be wary of thwarting their budgets in the process.

More than a quarter (27%) of Americans surveyed said that their most expensive gift was bought for a child.

More millennials took on holiday debt than any other age group, at 39%. That’s compared to 35% of Gen X, 30% of Gen Z and 17% of baby boomers.

“It’s no secret that millennials have been hit particularly hard by the pandemic,” Schulz said. “So many of them are already struggling with student loan debt, the costs of starting a family and other such financial headwinds that I’m not surprised to hear that many will be taking on more debt this holiday season.”

Click through to see previous versions of this annual report:

MagnifyMoney commissioned Qualtrics to conduct an online survey of 1,171 Americans, including 359 who incurred holiday debt. The survey was administered using a non-probability-based sample, and quotas were used to ensure the sample base represented the overall population. All responses were reviewed by researchers for quality control.

We defined generations as the following ages in 2020:

While the survey also included consumers from the silent generation (defined as those 75 and older), the sample size was too small to include findings related to that group in the generational breakdowns.

The survey was fielded Dec. 21-22, 2020.

Erika Giovanetti

Erika GiovanettiErika Giovanetti is the debt and personal loans writer for LendingTree. She has reported on a multitude of subjects, from personal finance to human interest to politics.

Read More